7-18

PRC : price per $100 of face value

CPN : coupon rate (%)

YLD : annual yield (%)

A : accrued days

M : number of coupon payments per year (1=annual, 2=semi annual)

N : number of coupon payments between settlement date and maturity date

RDV : redemption price or call price per $100 of face value

D : number of days in coupon period where settlement occurs

B : number of days from settlement date until next coupon payment date = D − A

INT : accrued interest

CST : price including interest

• For one or fewer coupon period to redemption

• For more than one coupon period to redemption

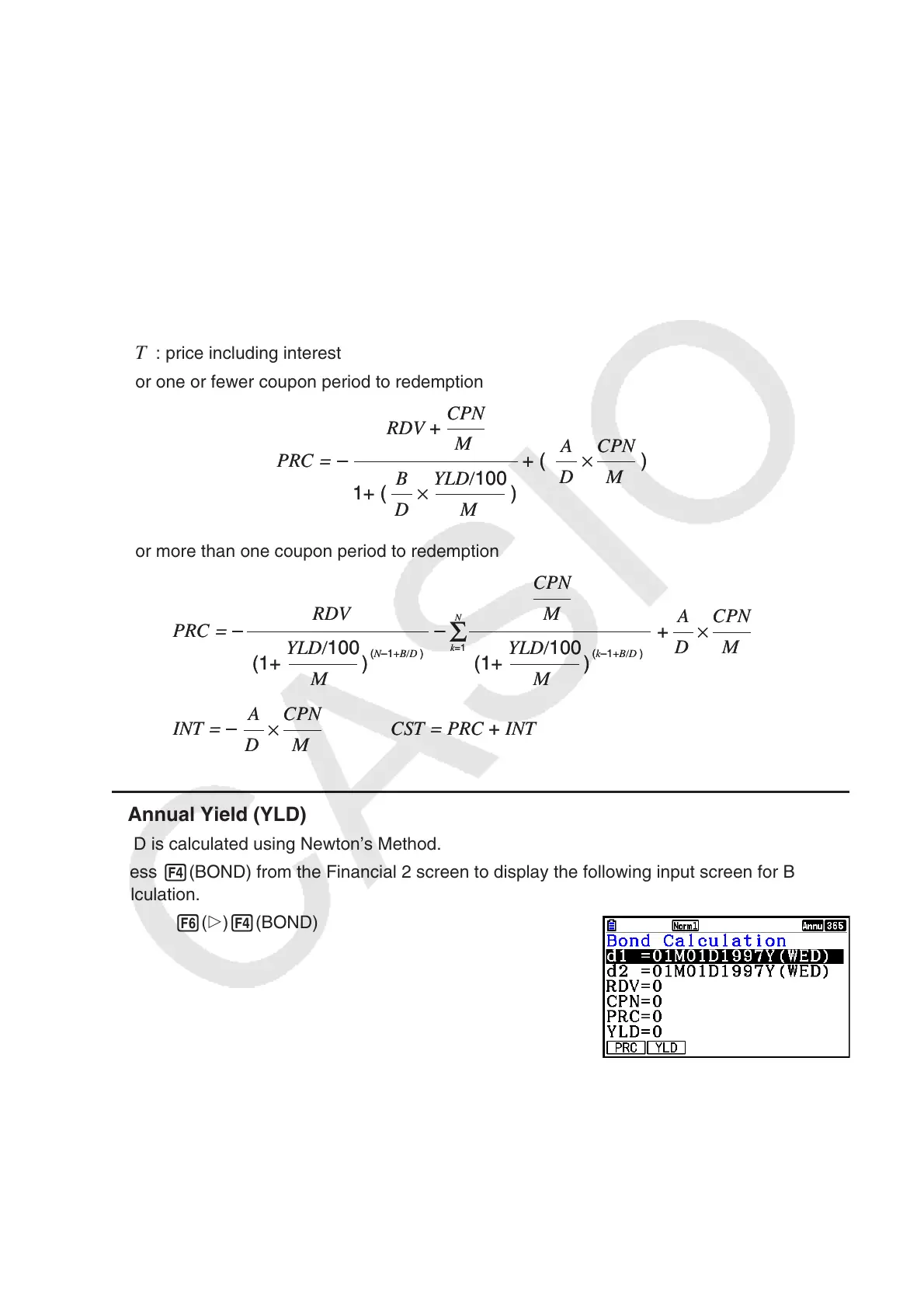

u Annual Yield (YLD)

YLD is calculated using Newton’s Method.

Press 4(BOND) from the Financial 2 screen to display the following input screen for Bond

calculation.

6( g) 4(BOND)

PRC = + (– )

RDV +

M

CPN

1+ ( × )

D

B

M

YLD/100

×

D

A

M

CPN

PRC = + (– )

RDV +

M

CPN

1+ ( × )

D

B

M

YLD/100

×

D

A

M

CPN

×

D

A

M

CPN

INT = – CST = PRC + INT

+

×

D

A

M

CP

PRC = – –

RDV

(1+ )

M

YLD/100

(1+ )

M

YLD/100

M

CPN

Σ

N

k=1

(N–1+B/D ) (k–1+B/D )

×

D

A

M

CPN

INT = – CST = PRC + INT

+

×

D

A

M

CP

PRC = – –

RDV

(1+ )

M

YLD/100

(1+ )

M

YLD/100

M

CPN

Σ

N

k=1

(N–1+B/D ) (k–1+B/D )